Managing Concentration Risk in a Retirement Portfolio

In this week’s Weekly Market Insights, we saw technology stocks once again lead broader market performance.

Strong momentum in artificial intelligence and growth companies pushed markets higher even as inflation remained sticky and economic growth slowed.

When one sector leads, it often feels like the place to be.

But for long-term investors, especially those nearing or in retirement, leadership concentration deserves a closer look.

Disclaimer: For informational and educational purposes only. Investment allocation and retirement income strategies should be tailored to your individual circumstances. Consult with your financial and tax professionals before making changes to your portfolio.

Key Takeaways

Market leadership rotates over time, often unpredictably

Strong recent performance can quietly increase portfolio concentration

Retirement portfolios need to manage sequence risk just as much as growth potential

Rebalancing helps maintain alignment with long-term objectives

Market Leadership Is Powerful and Temporary

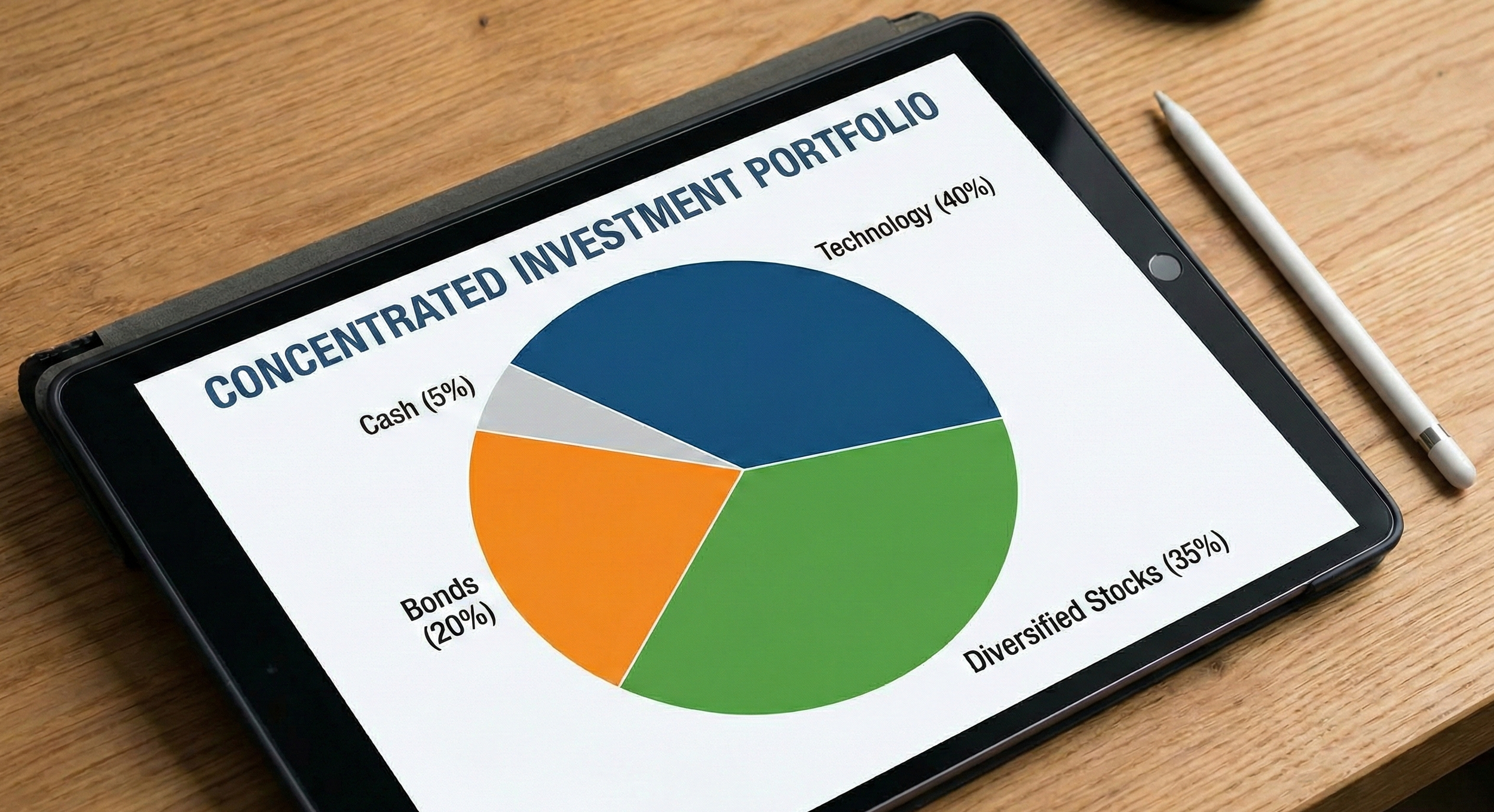

Technology and AI-driven companies have delivered strong returns in recent years. That momentum can naturally increase their weight inside diversified portfolios, even without adding new money.

This is how concentration builds quietly.

An asset class that performs well begins to represent a larger percentage of total portfolio value. Over time, what started as a balanced allocation can become tilted toward a single driver of returns.

Leadership feels permanent when you are in it. History shows it rarely is.

Small caps, international stocks, real estate, energy, and large cap growth have all had periods of dominance. None have remained on top indefinitely.

Why Concentration Risk Matters More in Retirement

For investors still accumulating assets, concentration risk can be uncomfortable but manageable. Time can smooth volatility.

Retirees face a different risk profile.

When withdrawals begin, the order of returns matters. A sharp pullback in a heavily concentrated sector early in retirement can magnify sequence risk, especially if income is being withdrawn at the same time.

This does not mean avoiding growth sectors. It means recognizing that retirement portfolios are designed to support income across many market environments, not just when one sector is thriving.

Rebalancing Is Discipline

Rebalancing often feels counterintuitive. You are choosing to sell the high performers in your portfolio and repurchase those that may have been lagging.

When technology is leading, trimming exposure can feel like stepping away from strength. When a sector is lagging, adding to it can feel uncomfortable.

But rebalancing is not about predicting which sector will outperform next.

It is about maintaining a risk level aligned with your long-term objectives.

Left unchecked, performance alone can shift the risk profile of a portfolio. Rebalancing brings it back in line with the original plan.

Helpful Insight 💡: A helpful way to think about rebalancing is that you are “cashing in” your winners. A portion of your portfolio exceeded expectations and now you are harvesting those gains to bolster your nest egg. This can be a good psychological way of viewing it.

Diversification Over Chasing Headlines

Headlines change weekly. Market leadership may change yearly. Investment plans should be built to endure both.

A properly structured retirement portfolio typically includes:

Growth assets to address long-term inflation

Defensive holdings to reduce volatility

Cash reserves to fund near-term income needs

Income-producing investments where appropriate

Each plays a role. No single sector carries the entire burden.

The Bigger Perspective

Strong performance from one sector is not a signal to panic or abandon it. It is simply a reminder to evaluate risk exposure through a long-term lens.

Market leadership rotates. Risk accumulates quietly. Discipline compounds over time.

The goal is not to own what is winning today. It is to own a portfolio that can support your goals across many tomorrows.