What to Do About 2026 TSP Changes

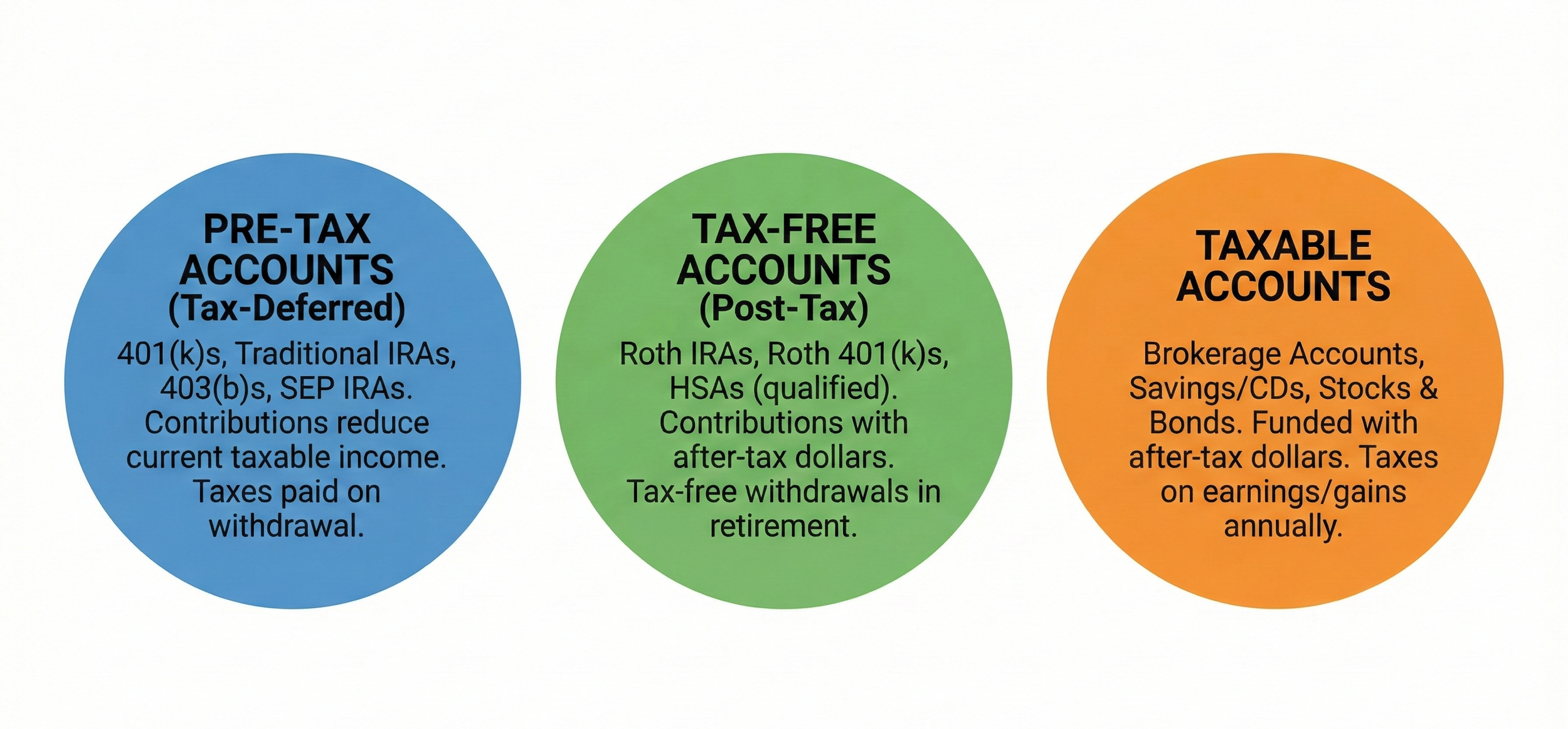

Several structural updates to the Thrift Savings Plan are now active in 2026. These updates directly influence tax positioning, contribution structure, and long term retirement income planning. When coordinated properly, they can expand flexibility.

Disclaimer: For informational and educational purposes only. Federal retirement benefits and tax laws are complex and subject to change. Consult with your tax or financial professional before making decisions related to your Thrift Savings Plan or retirement strategy.

Key Takeaways

Roth in-plan conversions are now available inside TSP

Higher earning employees age 50 and older must make Roth catch-up contributions

Tax planning is now more integrated into TSP contribution and distribution strategy

Retirement planning for federal employees should begin well before separation from service

Roth In-Plan Conversions Are Now Available

As of 2026, TSP participants can convert traditional balances to Roth directly inside the plan.

Here is how the rule works:

You elect the portion of your traditional TSP balance to convert.

The converted amount is included in taxable income for that year.

Once converted, those dollars grow tax-free.

Qualified withdrawals in retirement are tax-free.

Previously, many federal employees needed to separate from service or move funds into an IRA to execute flexible Roth conversion strategies. That additional step is no longer required.

This creates meaningful tax planning flexibility. Federal employees can now evaluate conversion opportunities during lower income years, early retirement before Social Security begins, or other transitional periods.

Roth Catch-Up Contributions Are Required for Higher Earners

Under the SECURE 2.0 Act, catch-up contributions now follow new rules for certain employees.

If your wages exceed the indexed income threshold, currently $145,000, catch-up contributions must be made on a Roth basis.

This means:

Employees age 50 and older may still contribute catch-up amounts.

If income exceeds the threshold, those catch-up dollars are after tax.

Qualified withdrawals of those Roth dollars in retirement are tax free.

For higher-earning federal employees, this automatically increases Roth exposure inside the TSP. While regular pre-tax deferrals are still permitted, catch-up contributions now shift account composition over time.

Tax diversification is no longer purely elective at higher income levels. It is partially embedded in the contribution structure.

Helpful Insight 💡: If a dual-income household was already near a tax bracket threshold, losing the pre-tax catch-up deduction could push income slightly higher into the next bracket due to the increase in marginal tax exposure on other income. NIIT exposure could be something to keep an eye on. This won’t be a dramatic spike, but it is something to monitor.

Planning Opportunities for Federal Employees

Evaluate Conversion Windows: Now that Roth in-plan conversions are available, timing becomes central.

Federal employees should evaluate:

Expected FERS pension start date

Social Security timing

Required minimum distribution age

Other pre-tax retirement balances

Years with temporarily lower taxable income may provide room to convert traditional TSP dollars at controlled tax rates. The opportunity is time sensitive. Missing it can permanently increase lifetime taxes.

Revisit Your Traditional and Roth Mix: Mandatory Roth catch-up contributions will gradually shift account composition.

For many FERS retirees, the pension creates a baseline of taxable income throughout retirement. That baseline often increases the long term value of tax free assets.

Rather than viewing Roth exposure as a regulatory outcome, it should be integrated into a deliberate tax diversification framework.

Just Because You Can Convert Does Not Mean You Should: Roth conversions are a tool. Like any tool, their value depends on timing, scale, and context. Every dollar converted is added to your taxable income in the year of conversion. That can:

Push income into a higher marginal bracket

Trigger Medicare premium surcharges later through IRMAA

Increase taxation of Social Security benefits

Reduce eligibility for certain credits or deductions

In some cases, paying tax today improves long-term efficiency. In other cases, accelerating income creates unnecessary friction.

The analysis should include:

Current marginal tax rate

Projected retirement tax bracket

Pension income floor under FERS

Timing of Social Security

Required minimum distributions

Engage in Planning Before Retirement, Not After: Comprehensive planning should begin years in advance to retirement. Some of the most meaningful decisions occur while you are still employed.

With the introduction of in-plan conversions, contribution structure, pension start dates, and Social Security coordination will be influenced by actions taken years before separation from service.

Working with a financial advisor and tax professional who understands federal benefits, including FERS, TSP, and FEHB, can provide clarity and coordination. The interaction between pension income, TSP withdrawals, tax brackets, and healthcare coverage is specific to federal employees.

Proactive planning during peak earning years allows for:

Multi-year tax bracket management

Strategic Roth positioning

Coordinated pension and withdrawal timing

More efficient transition planning

The Larger Retirement Framework

The 2026 TSP updates add flexibility inside an already strong retirement system. What they introduce is more room for tax coordination and long term structuring.

For federal employees, retirement income typically involves multiple layers:

The FERS pension

TSP balances

Social Security

FEHB coverage

Multi-year tax bracket management

Each of those components interacts with the others. A Roth conversion decision today can influence Medicare premiums later. Contribution structure affects future required distributions. Allocation decisions shape withdrawal flexibility.

The rule changes themselves are straightforward. The coordination is where planning becomes meaningful.

Many of the decisions that shape retirement outcomes are made years before separation from service. Having clarity on how these pieces fit together while still employed allows for a more intentional transition into retirement.