Weekly: AI Fears and Mixed Data

Stocks declined last week as investors reacted to mixed economic data and growing concerns that artificial intelligence could disrupt established business models across multiple sectors. While U.S. indexes moved lower, developed international markets posted gains.

Key Takeaways

AI disruption concerns spread beyond technology and pressured multiple sectors

Mixed retail, employment, and inflation data complicated the economic narrative

A midweek rally faded as investors reassessed jobs data beneath the headline number

Cooling inflation late in the week helped stabilize sentiment

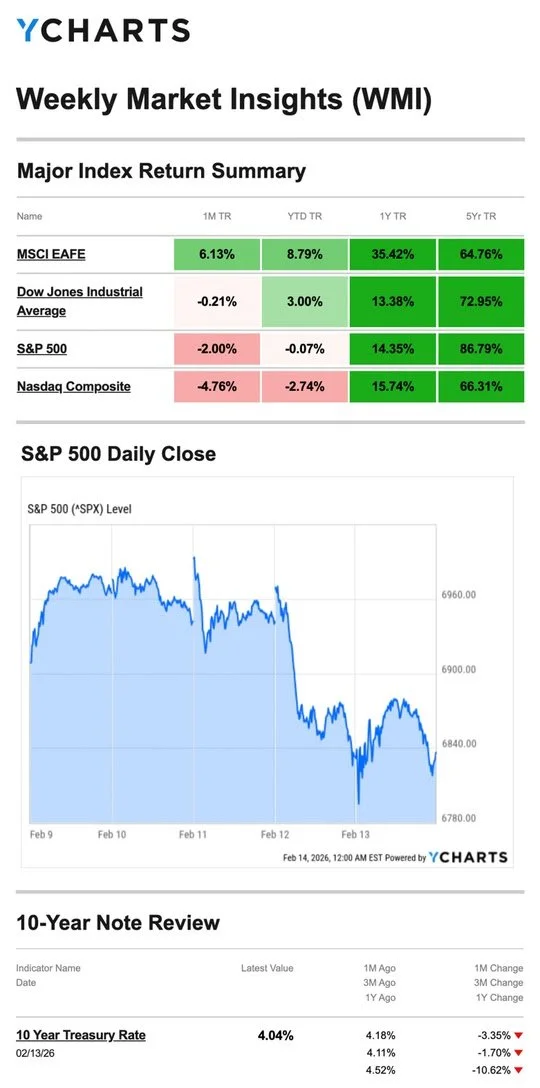

Source: YCharts.com, February 14, 2026. Weekly performance is measured from Monday, February 9, to Friday, February 13.

Market Performance Snapshot

The S&P 500 Index declined 1.39% for the week, while the Nasdaq Composite fell 2.1%, reflecting renewed pressure on technology and growth-oriented stocks. The Dow Jones Industrial Average slid 1.23%, as weakness broadened beyond the largest tech names.

In contrast, developed international stocks advanced, with the MSCI EAFE Index rising 1.92%. The divergence highlights continued rotation beneath the surface, with global markets and select non-technology sectors showing relative resilience even as U.S. indexes moved lower.

Weekly trading was marked by sharp midweek swings, as markets reacted quickly to retail sales, employment revisions, and inflation data.

AI Disruption Moves to Center Stage

Technology stocks began the week with modest gains, helping lift the Nasdaq and S&P 500 as investors maintained cautious optimism around earnings and economic growth.

That tone shifted after flat December retail sales raised questions about consumer momentum. At the same time, concerns grew that artificial intelligence could disrupt business models beyond traditional technology companies. Financial stocks were among the groups facing renewed scrutiny as investors evaluated how automation and AI tools may affect employment trends and operating models.

A stronger-than-expected January jobs report briefly lifted markets midweek. However, momentum faded as investors dug into the details, including downward revisions to prior data and uneven sector participation.

Good News, Bad News in the Data

Three major reports shaped the week: retail sales, employment, and inflation.

Retail Sales: Consumer spending was flat in December, below expectations and below November’s growth rate. With consumer spending representing a large share of economic activity, weaker momentum may influence how the Federal Reserve views its current policy stance.

Employment: January job gains exceeded expectations and the unemployment rate edged lower. However, downward revisions showed significantly fewer jobs were added over the prior year than previously estimated, and job growth was concentrated in a limited number of sectors.

Inflation: January inflation came in cooler than expected. The Consumer Price Index rose 2.4 percent year over year, down from 2.7 percent in December. While inflation remains above the Fed’s target, the slower pace helped markets rebound on Friday.

This Week: Key Economic Data

Monday

Markets closed for Presidents’ Day

Tuesday

Empire State Manufacturing Survey

Wednesday

Housing Starts (November, December)

Building Permits (November, December)

Durable Goods (December)

Trade Balance in Goods (December)

Retail Inventories (December)

Wholesale Inventories (December)

Federal Open Market Committee Meeting Notes (January)

Thursday

Weekly Jobless Claims

Trade Deficit (December)

Pending Home Sales

Minneapolis Fed President Neel Kashkari speaks

Friday

Gross Domestic Product (GDP), Q4

Personal Consumption Expenditures (PCE) Index (December)

New Home Sales (November, December)

Consumer Sentiment

This Week: Companies Reporting Earnings

Tuesday

Medtronic (MDT)

Palo Alto Networks, Inc. (PANW)

Constellation Energy Corporation (CEG)

Cadence Design Systems, Inc. (CDNS)

Wednesday

Analog Devices, Inc. (ADI)

Booking Holdings Inc. (BKNG)

Carvana Co. (CVNA)

DoorDash, Inc. (DASH)

Moody’s Corporation (MCO)

Thursday

Walmart Inc. (WMT)

Deere & Company (DE)

Newmont Corporation (NEM)

The Southern Company (SO)

Olivia throws a softball as hard as she can, and even though it doesn’t touch anything and nobody touches it, the softball comes right back to her. How is this possible?

Last Week's Riddle: It can be less thick than your finger when it folds, yet as thick as what it carries when it holds. What is it?

Answer: A sack.

Footnotes And Sources

1. WSJ.com, February 13, 2026

2. Investing.com, February 13, 2026

3. CNBC.com, February 9, 2026

4. CNBC.com, February 10, 2026

5. CNBC.com, February 12, 2026

6. WSJ.com, February 13, 2026

7. CNBC.com, February 10, 2026

8. WSJ.com, February 11, 2026

9. WSJ.com, February 13, 2026

10. IRS.gov, May 29, 2023

11. Investors Business Daily, Econoday economic calendar, February 13, 2026.

12. Zacks, February 13, 2026.

This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with Bethesda Wealth Planning Group.