Chart of the Month: February

Inflation shows up differently depending on how you spend.

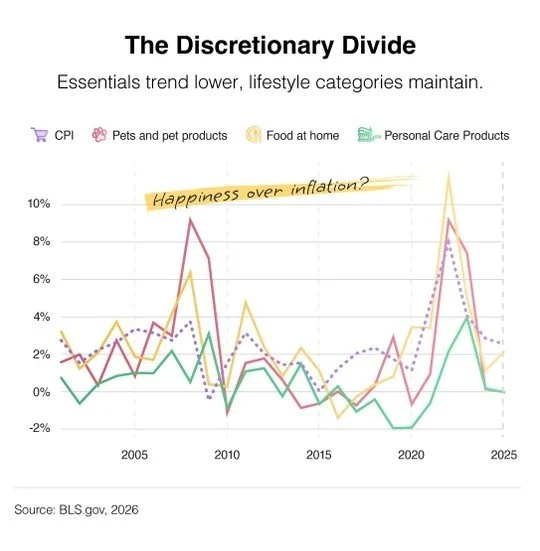

This month’s chart uses Bureau of Labor Statistics data to track 25 years of price changes across three everyday spending categories and compares them to headline CPI, the government’s broad measure of inflation.

Two of the three categories came in below headline CPI over the full period. One did not.

The difference helps explain why inflation can feel very personal.

Key Takeaways

Headline CPI does not reflect every household’s lived experience

Some categories rise more slowly than overall inflation over time

Others can spike sharply and feel far worse than the national average

Retirement planning must account for category-specific inflation

Pet Care

The price spikes in pet care during 2022 and 2023 were noticeable.

However, when stretched across 25 years, the long-term picture is more measured. According to the chart, $20 spent on pet products in 2001 would cost approximately $32.80 today. Under headline CPI, that same $20 would cost roughly $36.28.

Despite recent increases, pet care costs trailed broader inflation over the full period.

Short-term spikes can distort perception. Long-term data provides context.

Personal Care Products

Personal care products followed a similar pattern, and even more consistently.

Prices came in below headline inflation in 24 of the past 25 years. In nine of those years, prices actually declined. A $20 purchase in 2001 rose to about $22.82 by 2025.

That cumulative increase is far below what many people assume when they hear the word inflation.

Groceries

Food at home tells a different story.

In 2022, grocery prices rose 11.4%. That was more than three percentage points above headline CPI, which itself reached 8%. For many households, that year felt considerably worse than the national average.

Groceries highlight an important reality. Some categories diverge meaningfully from the broader index. When that category represents a large share of your budget, inflation feels amplified.

What This Means for You

Inflation lands differently depending on how you spend.

A retiree with higher healthcare costs will experience inflation differently from a young family focused on groceries. A renter will feel it differently than a homeowner with a fixed mortgage. A pet owner may notice spikes in veterinary services more than changes in apparel prices.

Over time, those differences compound.

This is especially important in retirement planning. Purchasing power erosion rarely happens all at once. It drifts gradually, category by category.

That is why we build retirement strategies with inflation assumptions tailored to your actual spending patterns rather than relying solely on headline CPI.